From voluntary to mandatory, are the ESG disclosure frameworks still fertile ground for unrealised EA career pathways? – A 2023 update on ESG potential impact

*Disclaimer: the author is employed by a major ESG rating firm. Therefore, opinions expressed in this post are solely those of the author and do not reflect or represent the position of the employer.

Acknowledgement

The completion of this post would not have been possible without the extensive insight, advice, and knowledge shared by the following individuals: Tomas Bueno dos Santos Momčilović, Yara Remppis, Dr. Jonathan Harris, Benjamin Yeoh, Sanjay Joshi, and Philip Chen. Any mistakes or oversights in this post are solely my responsibility.

Introduction

This post is written partly as a reflection towards my very own attempt to do the most good at early career, a literature review on the potential impact of working in sustainable finance, and how various thinkers within the Effective Altruism community have proposed their pathways to impact. I remember stumbling upon Sanjay Joshi’s $100 trillion dollar opportunity post (Joshi S., 2021) on why more EA should consider a career in ESG (Environment, Social and Governance) to maximise their impact. Back then, I was a young undergraduate finishing his degree in Geography, with a particular focus on Glacial Geomorphology. Partly for the fascination of ice and the urgency to combat climate change. I’ve come to realise that in order to have any actual impact in the realm of climate science, I would have to not only finish my PhD, do multiple postdocs, and secure a tenured position in order to contribute towards any significant research.

Given the current pace of climate change, by the time I could potentially achieve tractable impact, we might as well have reached 2 degrees warming if things progressed as predicted. This realisation, along with the understanding that addressing climate change is feasible and not as overlooked as previously thought (Hilton B., 2022, Buchner et al., 2021), have convinced me that change is already well underway institutionally. In the report Global Landscape of Climate Finance 2021, although there is still a significant investment gap between inflow investment and estimated need to maintain the 1.5 oC pathway, and climate investment in advanced economies are primarily funded by private capital (Buchner et al., 2021). Therefore, the most impact would be to amplify the already dominant market pull effect from the private sector.

The idea of making a meaningful difference in the private market, where a consensus framework is already established, is compelling. It implies that the wheel need not be reinvented. In this post, I will attempt to first bring the reader up to speed with the progress ESG have made, review the various theories proposed by Effective Altruists on the potential impact of ESG within the broader financial services landscape. I will then discuss the short-comings of the current frameworks and propose pathways to enhance impact for EA cause areas building upon the work that has been done within and beyond our community.

Part 1: If Climate Change is not neglected, why work in ESG, and how does ESG work?

Despite the greenwashing and various scandals, ESG investing has gained significant traction. ESG related funds gained $87 billion in the first quarter of 2022, and followed by a growth of $33 billion in the second quarter according to the most recent McKinsey report (Perez et al., 2023). Even with the recent setbacks caused by the Ukraine-Russian conflict, the longer term growth trajectory is promising, especially when some much effort and money have already been poured in. While it is true that current impact is marred by maligned or imperfect practices, the ESG industry remains a formidable force in the financial world. Not to mention the additional impact EAs could make from the “earning to give” pathways.

So let’s begin by talking about how ESG “works”.

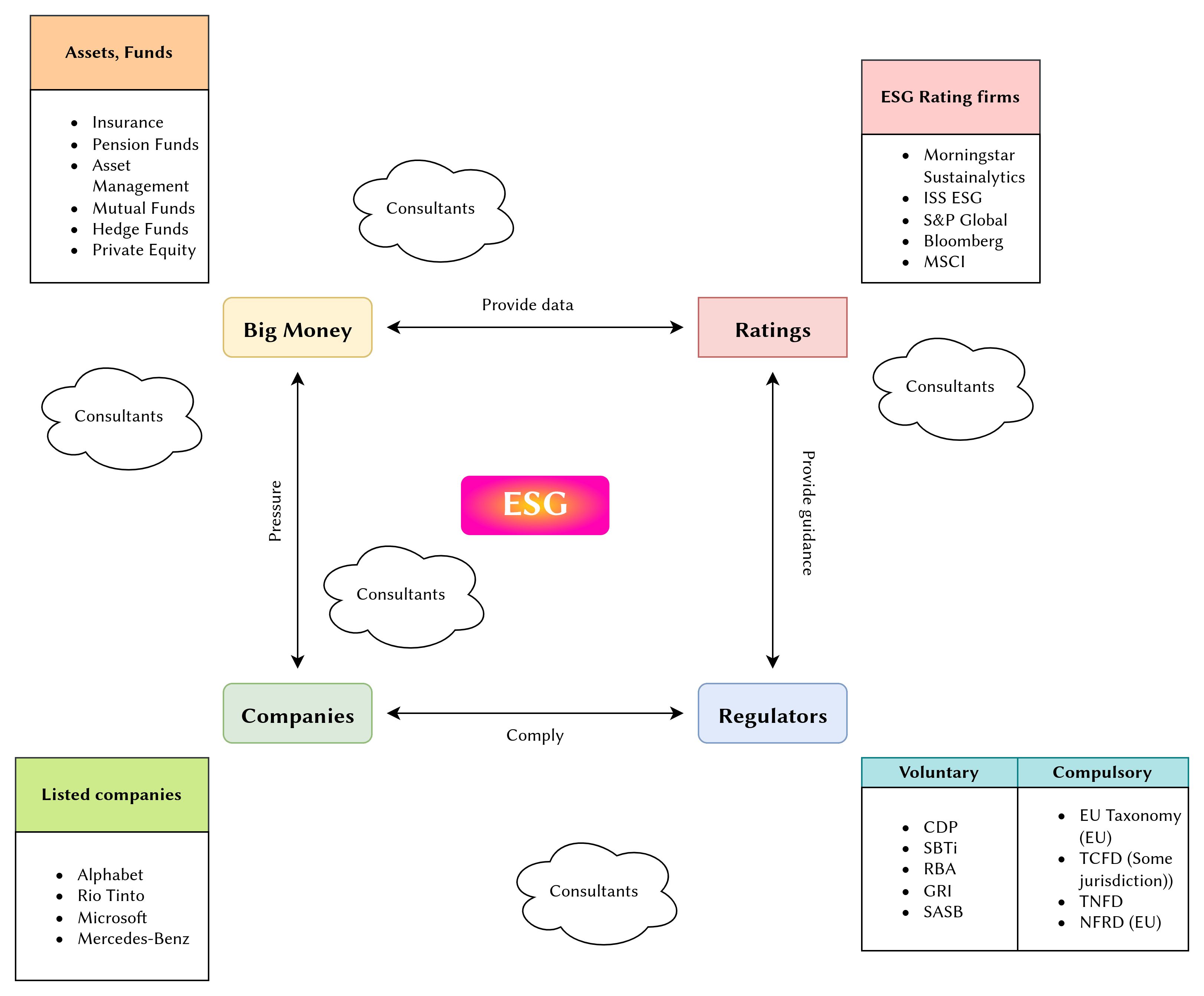

Figure 1. Schematic diagram on how various stakeholders in the ESG finance world relate to each other

This diagram illustrates the very simplified map of the relationship within the ESG world. There are four main stakeholder groups and their incentives are as follow: Companies are financed by investment from the largest funds, these include state funds, pension funds, and large investment banks with Assets Under Management (AUM) ranging from multiple billion well into multi trillion USD (colloquially known as Big Money). As our society both culturally and legally have started requesting for good behaviour from the private sector, large funds are therefore incentivised to invest in companies that appear good in order to attract retail investors and fulfil their fiduciary duty. In order to do this, large funds and investors purchase ratings and advice from ESG ratings agencies in an attempt to receive equitable advice on how prospective investments are performing or disclosing their sustainable activities. These ESG ratings agencies essentially model their data collection and ratings method on regulators from voluntary and/or compulsory disclosure schemes (e.g. TCFD, TNFD, EU Taxonomy).

So where’s the problem? Why isn’t this working?

Let’s delve into three instances where the ESG industry misses the mark for maximising impact. The first issue is greenwashing. To appeal to retail investors, Big Money must strike a balance between the interest of promoting good practice while ensuring an attractive financial return, a convenient and common strategy is through greenwashing (Raghunandan & Rajgopal, 2022, Roy et al., 2022). For example, when an advertised ESG fund contains less weightings of poor ESG performance companies but retain them for their profitability, or an ESG fund that is heavily skewed towards technology firms to limit their exposures. The second issue is the inconsistency of rating scores among ESG ratings providers (Prall K., 2021, Schmidt & Zhang., 2021). While there is a degree of interoperability among various ESG ratings providers in ways that they collect information (aka. factors), there is a lack of standardisation in how they conduct their ratings. Often. ESG ratings providers see an opportunity to differentiate by claiming to have more stringent assessment or data collection criteria than their competitors to attract clients. Lastly there is the problem of specification gaming (Yes, I am borrowing an AI-alignment concept). ESG ratings are often based on the quantity of disclosures rather than actual sustainability improvements. This has led to instances where companies would exploit the system, providing an illusion of good practice through extensive disclosure, while not actually achieving substantial improvements in sustainability (Raghunandan & Rajgopal, 2022).

If we compare the correlation of the major ESG ratings providers, the result might as well be stochastic.

Figure 2. ESG ratings comparison: correlations (Prall K., 2021)

Figure 3. Detailed ESG rating comparison between Morningstar Sustainalytics and S&P Global (Prall K., 2021)

For more information, see the opinion piece Lies, damned lies and ESG rating methodologies published by the Financial Times (Allen K., 2018).

Part 2: Directing ESG Impact: Current EA Theories and Efforts

Since 2021, there’s been an increasing amount of posts trying to address this potentially high impact career path. However, contribution remains limited to the few authors if you do a quick search on the forum. Current topics range from capturing better data for the Environmental pillar and embedding it into the valuation process to quantitatively calculating the potential impact adjusted returns for altruistic investors.

Better Climate Data

Currently, most if not all scientists, if they ever venture into sustainable finance, remain in short term risk assessments for the insurance and reinsurance industry. As it is much easier to calculate risks locally and regionally. In Philip Chen (2022) post, he suggested that better usage of climate modelling data could help build medium-term climate risk into the business valuation process. Holding companies accountable like they would by their valuation on their balance sheet. He also proposed that innovative financial products could be built such as a locust bond which would payout a sum of money when successfully controlled for a natural catastrophe induced by climate change.

Universal Ownership

Key people such as Sanjay Joshi, Ellen Quigley, and Thomas O’Neill have been championing a concept called Universal Ownership. Essentially, Universal Owners are the “Biggest Money” with multi trillion, international, diversified portfolios. Since they invest in such a broad range of society, any mis-behaviour in particular groups of bad companies could contribute to the economic cost for the rest of their portfolio (Quigley E., 2019 & Joshi S., 2023). A hypothetical example would be a fund invested in both biotechnology and lab equipment manufacturing. If their biotechnology investment has been involved in conducting unethical research, resulting in an international sanction. This could harm the financial return of their lab equipment manufacturing holdings whether through sanction for being the suppliers or loss of business from reputational damage.

The rise of mass retail investment and passive investing, caused by the popularity of low-cost online brokerages such as Interactive Brokers, eToro, and SAXO etc. has theoretically expanded the pool of Universal Owners significantly (Quigley E., 2019). This new group of Universal Owners are predominantly from a younger demographic who care more about corporate responsibility, and can potentially exercise much power collectively; examples of UO action theories could be found in the relevant posts.

Total Portfolio Project

The Total Portfolio Project (TPP) is a non-profit initiative that was established to guide impact-aligned investors, EA and otherwise. The project hopes to assist altruistic investors in optimising their portfolio, encompassing both traditional investments and grants. In addition to ESG-related topics, they have also done investigations into topics like “Setting Optimal Giving Rates” and “Mission-Correlated Investing”. Their work on “Impact Returns” has the most relevance to ESG.

“Impact Returns” represents the neglected, non-financial ESG contribution of an investment which can be combined with the financial returns to guide an altruistic investment decision:

“This investment has a 15% financial return plus a 5% impact return, for an impact-adjusted return of 20%. Given my goals, this is better than an alternative investment with a 19% return (e.g. 19% financial return + 0% impact return) for the same risk.” (TPP, 2023)

TPP has identified three keys to assessing valid impact returns for an investment:

Account for the magnitude of the underlying project.

Adjust for the number of interested investors and the project’s room for more funding to get an estimate of the actual contribution needed for said investment. Their methodology is similar to the approach discussed by Paul Christiano (2019) post.

Translate the impact into a financial value by multiplying it by the estimated cost-effectiveness of a benchmark grant, such as those given to GiveWell top charities (if the cause area is a global health impact).

For investors looking to incorporate ESG information into their portfolio in an impact-aligned way, the “Impact Returns” can be used to assign weightings to their investments.

Figure 4. Considering impact returns and financial returns allows impact-aligned investors to split the investment landscape into investments they should include or exclude in their optimal portfolio (TPP, 2023). I highly recommend going through the visual intro on the TPP website to get a better understanding.

To conclude, the discussion of ESG investment in the EA community is modest but diverse. Contributors coming from various domain expertise of the financial industry have shown the immense potential for a career in ESG finance to have significant impact.

Part 3: Adapting ESG for Longtermist EA Causes

Now that we have established the foundation and explored current theories and efforts. The rest of the post will be dedicated to suggesting how we can harness the current ESG framework to benefit longtermist cause areas. Demonstrating that a career path in ESG finance could go beyond current superficial impact and earning to give.

The EU Artificial Intelligence Act conformity assessment and other voluntary disclosures

The discussion of AI governance and AI alignment within the EA community generally consider the impact of Artificial Intelligence to be a longtermist cause area. Yet creating a short-term regulatory approach could really help establish a roadmap for longtermist AI governance. If we draw an analogy to the other EA longtermist cause area such as nuclear disarmament, we could see the transition of regulation and rules from short-term focus disarmament guidance towards a longer-term safeguard verification practice. The International Atomic Energy Agency (IAEA) was established in the wake of WW2 to promote and control the use of nuclear technology (Fischer D., 1997). The enforcement of Article III of the Treaty on The Non-Proliferation of Nuclear Weapons (NPT) was first limited to preventing development of nuclear technology. Against many sceptics of the time, the NPT responsibility was further extended in 1970, where verification processes were put in place for any activity involving the enrichment, storage, and disposal of Uranium and Plutonium. By 1995, the NPT was extended indefinitely and subsequent safeguard requirements have continued to evolve since (Rockwood L., 2013).

As part of the EU Artificial Intelligence Act development (EUAIA), the CEN-CENELEC which is the European Committee for Standardisation focus group is responsible for establishing a harmonising standard disclosure process along various AI-safety themes (CEN-CENELEC, 2020). The focus group aims to steward the standardisation of compliance protocols among the European member states. The 7 themes to be addressed for standardisation were:

Accountability

Quality

Data for AI

Security and privacy

Ethics

Engineering of AI systems

Safety of AI systems

Figure 5. The continuous reviewed cycle of standardisation and legislation to ensure relevance of the legally-binding act (CEN-CENELEC, 2020)

With standardisation in place, voluntary and compulsory disclosures are already being developed. The CapAI conformity assessment procedures was developed by the University of Oxford Saïd Business School (Floridi et al., 2022) to guide compliance for the legally-binding EUAIA. The EUAIA proposed GDPR-like penalties to non-compliance (European Commission, 2021). Other jurisdiction are also coming up with their respective ethical AI framework that could potentially become voluntary or compulsory disclosures (e.g. NIST’s AI Risk Management Framework 1.0).

An ESG like near-term AI-Governance factor collection could look like this:

Factor | Answer |

|---|---|

| Does the company engage in high-risk AI development? |

|

| If the company does engage in high-risk AI development, does the company participate in disclosures or guidelines, if so, which? |

|

| Does the company publish data-bias report, if so, how often? |

|

Table 1. A non-exhaustive example of factor questionnaire which mirrors how ESG data is collected.

There are already new start-ups that are trying to capture the AI-governance market. HolisticAI and Z-inspection for example are working in data-bias reporting, mitigations, and model interpretability. We can expect an ecosystem of compliance related industry to emerge in the coming years as reporting practice matures.

The development of such frameworks is encouraging and does mirror the evolution of voluntary and compulsory disclosure in ESG. I posit that the framework of factor questionnaire, tick-box approach, currently employed in ESG data collection can be easily adapted for reporting on the new AI governance frameworks. Perhaps, an AI-alignment score could soon be a feature of your nearest ESG fund. Moreover, AI companies might also swiftly devise strategies of “specification gaming” in relation to AI-alignment disclosures.

Part 4: Can sustainable finance outside the ESG framework potentially account for longtermism?

Increasingly, these ESG contexts have been incorporated into executive (C-Suite) compensation, although adaptation is still superficial at best (Spierings M., 2022).

Figure 6. Various motivations to incorporate ESG targets as part of compensation package (Spiering M., 2022)

Stakeholder capitalism and shareholder activism could have a high potential to change this! If proxy advisory firms could be influenced to consider concepts and advice along the Universal Ownership or Total Portfolio Project, they could play a major role in pressuring companies and boards to couple their compensation plan with a wider range of ESG metrics and move into longtermist causes. This would hopefully start with incorporating near-term AI-alignment into tractable advice. Proxy firms such as Institutional Shareholder Services and Glass Lewis are in a unique position to leverage this. If you are not familiar with proxy advisory service, see this news about Musk tweets proxy voting firms have ‘far too much power’ | Reuters.

Conclusion

ESG data solutions have made strides as evidenced in the diverse sets of disclosures whether voluntary or mandatory. However, challenges in ratings inconsistencies and the general shorttermist focus of data collection method have limited its potential impact. Given the nascent nature of ESG data, which currently value breadth over frequency, it is difficult to model it against financial returns.

The existing framework of factor-based questionnaires and the resulting ratings could be invaluable in the near-term governance of longtermist cause areas if controlled for “specification gaming”. This post has explored how the EU Artificial Intelligence Act (EUAIA) could potentially be aligned with this framework. While this post has focused on the intersection of ESG and AI governance, it’s worth noting that similar approaches could potentially extend to other longtermist cause areas, such as biosecurity and pandemic preparedness. Although these areas are outside my expertise, they represent exciting avenues for future exploration and discussion.

Contact

Feel free to provide comments, thoughts, and criticism in the comment boxes below or contact me at chrischank{at}protonmail{dot}ch. Thank you for reading.

Bibliography

Allen, K., 2018. Lies, damned lies and ESG rating methodologies. Financial Times.

Barbara Buchner, Baysa Naran, Pedro Fernandes, Rajashree Padmanabhi, Paul Rosane, Matthew Solomon, Sean Stout, Costanza Strinati, Rowena Tolentino, Githungo Wakaba,, Yaxin Zhu, Chavi Meattle, Sandra Guzmán., 2021. Global Landscape of Climate Finance 2021. Climate Policy Initiative.

Buchetti, B., Arduino, F.R., De Vito, A., 2022. A Systematic Literature Review on Corporate Governance and ESG research: Trends and Future directions. https://doi.org/10.2139/ssrn.4286866

CEN-CENELEC, 2020. Road Map on Artificial Intelligence (AI). CEN-CENELEC.

Chen, P., 2022. Leveraging finance to increase resilience to GCRs. URL https://forum.effectivealtruism.org/posts/fHfuoGZc5hqfYTwMH/leveraging-finance-to-increase-resilience-to-gcrs (accessed 5.14.23).

Christiano, P., 2019. Analyzing divestment. The sideways view. URL https://sideways-view.com/2019/05/25/analyzing-divestment/ (accessed 6.3.23).

European Commission, 2021. Proposal for a REGULATION OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL LAYING DOWN HARMONISED RULES ON ARTIFICIAL INTELLIGENCE (ARTIFICIAL INTELLIGENCE ACT) AND AMENDING CERTAIN UNION LEGISLATIVE ACTS, 52021PC0206.

European Commission, 2020. The Assessment List for Trustworthy AI (ALTAI) for self assessment (No. KK-02-20-479-EN-C). European Commission, Brussels.

Fischer, D., 1997. History of the international atomic energy agency. The first forty years. IAEA, Vienna.

Floridi, L., Holweg, M., Taddeo, M., Amaya Silva, J., Mökander, J., Wen, Y., 2022. capAI—A Procedure for Conducting Conformity Assessment of AI Systems in Line with the EU Artificial Intelligence Act. https://doi.org/10.2139/ssrn.4064091

Harris, J., 2021. A Framework for Investing with Altruism. https://doi.org/10.2139/ssrn.3934090

Harris, J., n.d. Total Portfolio Project [WWW Document]. URL https://www.total-portfolio.org/ (accessed 5.31.23).

Hilton, B., 2022. Climate change—Problem profile—EA Forum. URL https://forum.effectivealtruism.org/posts/DmshhvanTb9wSh5x6/climate-change-problem-profile#Neglectedness__ (accessed 5.23.23).

Joshi, S., 2021. The $100trn opportunity: ESG investing should be a top priority for EA careers—EA Forum. URL https://forum.effectivealtruism.org/posts/4vRdt9Z9LsmaP7dHY/the-usd100trn-opportunity-esg-investing-should-be-a-top (accessed 5.23.23).

Joshi, S., n.d. This innovative finance concept might go a long way to solving the world’s biggest problems. URL https://forum.effectivealtruism.org/posts/ZCugsfAfZiYuQ8wfA/this-innovative-finance-concept-might-go-a-long-way-to (accessed 5.10.23).

NIST, 2023. Artificial Intelligence Risk Management Framework (AI RMF 1.0) (No. NIST AI 100-1). National Institute of Standards and Technology, Gaithersburg.

Pérez, L., Hunt, V., Samandari, H., Nuttall, R., Biniek, K., n.d. Does ESG really matter— and why? McKinsey.

Prall, K., 2021. ESG Ratings: Navigating Through the Haze. CFA Institute Enterprising Investor. URL https://blogs.cfainstitute.org/investor/2021/08/10/esg-ratings-navigating-through-the-haze/ (accessed 5.10.23).

Quigley, E., 2019. Universal Ownership in the Anthropocene. https://doi.org/10.2139/ssrn.3457205

Raghunandan, A., Rajgopal, S., 2022. Do ESG Funds Make Stakeholder-Friendly Investments? https://doi.org/10.2139/ssrn.3826357

Rockwood, L., 2013. Legal framework for IAEA safeguards.

Roy, A., Cohen, B., Scholz-Bright, R., Skinner, R., Davison, W., 2022. Litigation Risks Posed by “Greenwashing” Claims for ESG Funds. The Harvard Law School Forum on Corporate Governance. URL https://corpgov.law.harvard.edu/2022/04/25/litigation-risks-posed-by-greenwashing-claims-for-esg-funds/ (accessed 6.3.23).

Schmidt, A.B., Zhang, X., 2021. Optimal ESG Portfolios: Which ESG Ratings to Use? https://doi.org/10.2139/ssrn.3859674

Spierings, M., 2022. Linking Executive Compensation to ESG Performance. The Harvard Law School Forum on Corporate Governance. URL https://corpgov.law.harvard.edu/2022/11/27/linking-executive-compensation-to-esg-performance/ (accessed 5.24.23).

Versace, C., Abssy, M., 2022. How Millennials and Gen Z Are Driving Growth Behind ESG [WWW Document]. URL https://www.nasdaq.com/articles/how-millennials-and-gen-z-are-driving-growth-behind-esg (accessed 6.3.23).

Thank you for this broad introduction to ESG in relation to EA. For people like me who know little about ESG, this is very informative.

One thing that strikes me is the comparison between EA charity evaluation and ESG rating. While charity evaluators focus on a very few charities who can provide comprehensive, quantitative data, I assume that ESG rating agencies attempt to rate every large company. While EA charity evaluators convert results to one metric (such as DALYs/$) to have a common currency to compare organizations, the impression I get is that ESG rating agencies aggregate many dimensions like teachers grade students: by combining some hybrid of absolute scales and relative scales (grading on the curve) into letter grades, which can then be averaged. While the measures that EA charity evaluators use, such as saving the most lives for the least money, are probably goals that most people would consider good and reasonable, ESG rating agencies have to lump together a wide variety of goals, each of which is valued across a wide spectrum by people in the world. Some of the goals may even be regarded negatively by substantial fractions of people, while high priorities of many people may be omitted from ESG goals.

So ESG rating seems far more ambitious and challenging than EA charity evaluation. But it may still be worth trying, because the impact might be very large.

It seems very difficult but perhaps valuable to try to overcome the problem of combining disparate dimensions by not resorting to qualitative letter grades, but instead by estimating quantitative effects using a single measure, like DALYs. Easier said than done, though.

Thanks for reading Larry,

Your assessment is generally correct, however just one more thing. In ESG ratings, we also take into consideration industry clusters so that companies are ranked against their peers as much as possible. Additionally, in order to have more dimensions, we not only use company self disclosure data but also watch for controversial news, lawsuits.

This means that which data to use and how to normalise or “curve” they grade it on is in the discretion of the industry experts within each ESG rating company.

Of course, at the end of the day, funds hold multiple industries. Which means that they eventually get aggregated so lose some of that granularity.

Great to see people writing about this topic, thank you. Thank you also for reaching out to discuss and for sharing a draft with me in advance. I’m sorry I wasn’t able to review it, I’ve been a bit under the weather of late.

As I’m still under the weather, I’ve only skimmed your post, so sorry if I’ve missed something. As this is a topic I’m interested in I would normally prefer to read more carefully. Some quick comments:

Your post mentions that “the longer term growth trajectory [for ESG] is promising”; I don’t think this does justice to the anti-ESG sentiment brewing in the US.

Minor comment: I’d say that your summary of ESG is skewed to your experience in ESG ratings. This is an important element of ESG, but there are other elements too.

I’m excited to see more content about the intersection of AI risk and ESG. I’ve been having a few conversations about this and I suspect there’s scope for high-impact work here.

You are absolutely correct, the perspective I have is quite narrow due to my lack of experience in the field. However, I hope this none-the-less help shed some light on the current ongoing projects and thoughts around the field. Moreover, I do realise the perspective on the post is very Euro-environment centric. I do not have expertise or experience in other markets to comment on them.

Thanks for writing this! Hoping to respond more fully later.

In the meantime: I really like the example of what a “near-term AI-Governance factor collection could look like”.